When it comes to investing, the financial media loves a thrilling narrative. Pundits debate the next breakout tech stock, analyze quarterly earnings down to the penny, and try to time the market’s daily swings. However, the somewhat unglamorous truth is that picking the “next big thing” isn’t what actually builds long-term wealth.

If you want to understand the true driver behind your investment success, you need to look at a much broader strategy: asset allocation.

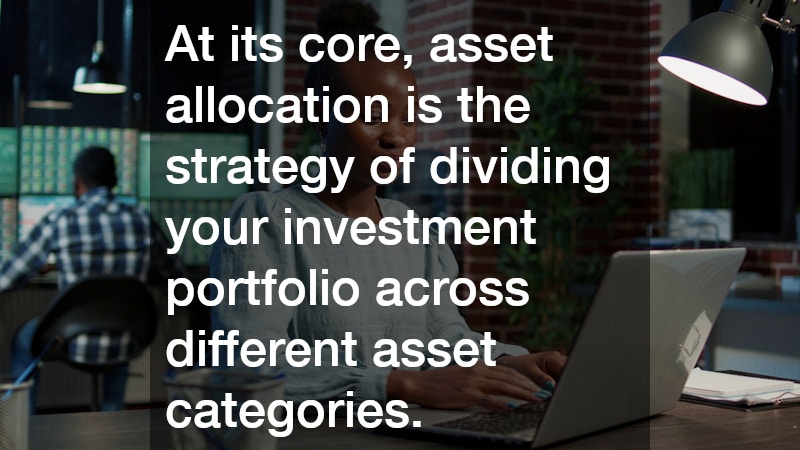

What Is Asset Allocation?

At its core, asset allocation is the strategy of dividing your investment portfolio across different asset categories. The most common primary categories include:

- Equities (Stocks): Representing ownership in companies. These offer the highest potential returns but come with the highest short-term volatility.

- Fixed Income (Bonds): Loans made to corporations or governments. These generally offer lower returns than stocks but provide stability and consistent income.

- Cash and Equivalents: Savings accounts, CDs, or money market funds. These are highly liquid and safe, but offer the lowest return, often failing to outpace inflation.

- Alternatives: Real estate, commodities, or private equity, used to further diversify away from traditional stock and bond markets.

The goal isn’t just to own different investments, but to own investments that behave differently under the same market conditions.

Why It Trumps Stock Picking

It is entirely natural to assume that the specific stocks or mutual funds you choose dictate your financial destiny. Yet, a landmark 1986 study by Brinson, Hood, and Beebower fundamentally changed how professionals view portfolio management.

The study revealed a shocking statistic: over 90% of the variance in a portfolio’s returns over time is determined by asset allocation. Market timing and individual stock selection accounted for less than 10% of the outcome. In other words, deciding to put 70% of your money in stocks and 30% in bonds is a vastly more consequential decision than deciding which specific stocks or bonds to buy.

The Ultimate Risk Management Tool

Beyond driving returns, determining your ideal asset mix is your primary defense against catastrophic loss. Markets are inherently cyclical. When equities enter a bear market, high-quality bonds often hold their value or even rise as investors flee to safety.

By holding a mix of non-correlated assets, you smooth out the bumpy ride of investing. This does more than just protect your capital; it protects your psyche. A well-allocated portfolio prevents the panic-selling that destroys wealth during market downturns.

How to Build Your Ideal Allocation

There is no universally perfect portfolio. Your ideal mix should be entirely tailored to your personal circumstances based on three key pillars:

- Time Horizon: When will you need the money? If you are investing for a retirement that is 30 years away, you can afford a stock-heavy portfolio because you have time to recover from market crashes. If you are buying a house in three years, that money belongs in cash or short-term bonds.

- Risk Tolerance: This is your psychological ability to endure losses. If a 20% drop in your portfolio’s value will cause you to lose sleep and sell at the bottom, you need a higher allocation of bonds, regardless of your age.

- Ongoing Rebalancing: Over time, market movements will shift your initial allocation. If stocks have a banner year, your 70/30 portfolio might drift to 80/20. Rebalancing—selling high-performing assets to buy underperforming ones—forces you to “buy low and sell high” while returning your portfolio to its intended risk level.

The Bottom Line

While the thrill of chasing individual stock winners is undeniable, successful investing is ultimately a game of strategy, not speculation. By focusing your energy on getting your asset allocation right, you build a sturdy financial house that can weather the inevitable economic storms, keeping you firmly on the path to your long-term goals.